In part 2 of the series on green building, we take a look at the current status of transformation towards sustainability in India and across the world

Indian context:

The world average construction rate is at 5.2% vis-a-vis India’s 10%. With vertical gardens, radiation cooling towers and geothermal insulation, the concept of green buildings has been slow but has certainly taken off in India. Buildings use about 20% of the total power in India with growth at 11-12% annually. The Energy Performance Index (EPI) of commercial buildings in India is 200 to 400 kWH/sq.m/year vs. Europe and US which is much lesser at 150kWH/sq.m/year. However, the Indian market sees a huge potential of about USD 365 million for developing green materials and equipment. In the next 3-4 years, India is projected to develop green space which includes 200 million sq ft of commercial space and 45 million retail space across metros. These buildings will reduce overall costs and carbon emissions along with giving a higher rental value than conventional ones coupled with an earning of carbon credits. The payback period is expected to be around 2-7 years depending upon certification.

Environmental regulations are one of the major drivers of the green growth in India. However there is a need for public incentives and public awareness to further drive this concept. Apart from environmental regulations, the right thing to do, healthier neighborhoods, employee recruitment along with lower operating costs are other driving factors for going green.

The government has launched the ‘Energy Conservation Building Code (ECBC)’ to promote green buildings in India. However, green buildings cost much higher in construction as they are still in a nascent stage, along with a lack of technical information and short term returns than ROI. Some of the first few green buildings in India are: CII-Sorabji Godrej GBC Hyderabad (2004), ITC Gurgaon, Wipro Gurgaon, Technopolis Kolkata, Spectral Services Consultants Noida, HITAM Hyderabad, TCS Technopark and Grundfos Pump Chennai, Turbo Energy Limited Chennai, Aquamall Water solutions Gulbarga, RMZ Ecospace Kolkata, Infosys Pocharam, Olympia Tech Park Chennai, Leela Palace New Delhi, RMZ Millenia Business Park Chennai, Suzlon One Earth Pune, ITC Royal Gardenia Bangalore.

World-wide phenomenon:

Global construction output is expected to increase by 2020. The global average of green construction projects is 24%; by countries such as South Africa, Singapore, India, Germany and Mexico. Apart from nations like US, UK and China which already have a high growth in green and sustainable buildings, Poland, Mexico, Brazil, Columbia, Saudi Arabia, Chile are indicated to be moving towards the green path. By 2018, Brazil’s green building activity will have increased six times from 2015 (6-36%), with China increasing by five times (5-28%) and Saudi Arabia four times (8-32%).

Also by 2018, many firms will have more that 60% of their projects going green, from the current 18% to 37% and this will mostly be visible in countries such as India (52%), Mexico (44%), South Africa (61%), China (28%), Brazil (36%)and Colombia (38%); followed by Singapore (38%), UK (31%) and US (39%). The demand for green buildings is growing by the day; 35% in 2012 to 40% in 2015, especially in UK, Singapore and India.

The top triggers are client demand, environment regulations, market demand, and it being a right thing to do. Client demand is high in US and Australia, while market demand is rising in UK and China. Environment regulations have deep influence in Australia, UK, Singapore and India. Doing the right thing is the driver in Singapore, China and South Africa. Low operating costs is the trigger in Saudi Arabia, Singapore and Brazil followed by Poland, South Africa and US.

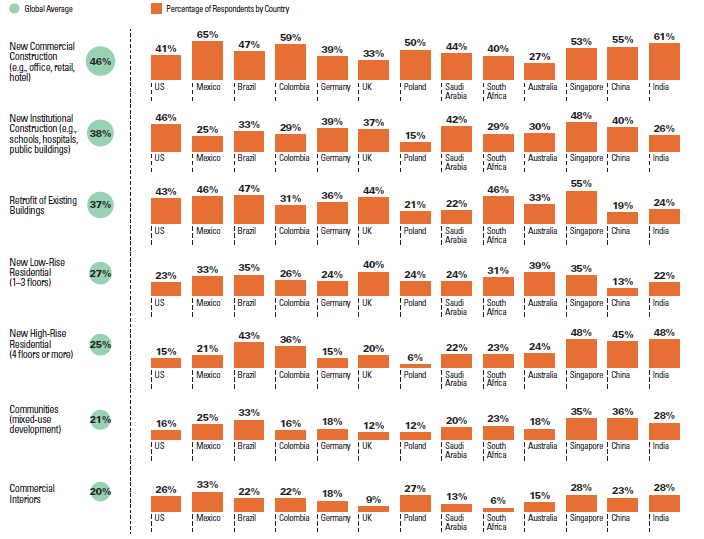

Sectors:

Sectors With Planned Green Activity Over the Next Three Years (Global Average and by Country)

Source: www.fidic.org

In the next and last part of this series, we bring to you an update on clean resources and the latest trends.

*All data courtesy Dodge report 2016